For years, Nvidia has held an ironclad grip on the AI hardware market. Its GPUs power the world’s most advanced AI models, and its CUDA software ecosystem has made switching to competitors feel nearly impossible. But as we move into 2026, something has changed. AMD is no longer just a distant runner-up, it has become a genuine strategic alternative for the world’s most powerful tech companies.

Hyperscalers like Meta, Microsoft, Google, and Amazon are spending hundreds of billions on compute, but they’re increasingly wary of depending on a single supplier. That fear of over-reliance has opened a door for AMD, landing deals worth a potential $150 billion and forging partnerships that would have seemed unthinkable just two years ago.

AMD’s stock reflected this turbulence. It surged past $260 early in 2026 before pulling back to around $195 after news of a deepened Nvidia-Meta partnership rattled investors. That volatility tells the story of this moment perfectly: the race for AI infrastructure dominance is intensely competitive, and no outcome is guaranteed.

The $150 Billion Anchor: Meta and OpenAI Go All-In

Meta has signed a multi-year agreement worth approximately $60 billion over five years, covering 6 gigawatts of compute capacity. To put that in perspective, 6 gigawatts is enough energy to power six million homes. Meta is deploying custom versions of AMD’s Instinct MI450 GPUs, specifically tuned for its Llama AI models.

OpenAI’s deal carries an even larger revenue ceiling: a cumulative hardware potential of $90 billion. Combined with Meta, AMD now has anchor customers that give it both financial security and a powerful market signal.

AMD CEO Lisa Su described the Meta collaboration as a “true win-win,” and it’s hard to argue otherwise. These deals don’t just fill AMD’s order book — they signal that the era of single-supplier dependence in AI is ending.

A Clever Twist: Turning Customers Into Shareholders

Perhaps the most inventive element of AMD’s strategy is how it has structured these partnerships. Rather than simply selling chips, AMD has granted OpenAI and Meta performance-based warrants a.k.a the right to purchase up to 160 million AMD shares at just $0.01 per share.

This isn’t a giveaway. The warrants only vest if these partners hit aggressive GPU shipment milestones and specific stock-price targets. The result is a powerful alignment of incentives: if AMD succeeds, its biggest customers benefit financially. That makes them genuinely motivated to optimize their software for AMD hardware, invest in the ecosystem, and keep buying chips.

It’s a masterstroke. Nvidia’s moat has always been partly relational, its customers are locked in by software, familiarity, and inertia. AMD is trying to create a different kind of lock-in: one built on shared equity upside. By making OpenAI and Meta potential shareholders representing up to 10% dilution, AMD transforms a vendor-customer relationship into a strategic alliance.

The Architecture Behind the Ambition: Zen 6 and 2nm

Big deals require big chips. AMD’s hardware ambitions rest on its next-generation “Zen 6” architecture, codenamed Venice. This is a ground-up redesign built for the demands of 2026’s AI data centers.

The headline spec is striking: up to 256 processor cores per chip, built on TSMC’s cutting-edge 2-nanometer manufacturing process. The move to 2nm is significant because it allows AMD to pack more transistors into less space, improving performance while reducing energy consumption, a critical factor when data centers are already straining power grids.

Zen 6 also introduces an 8-wide dispatch engine, a design that allows workloads to use processing resources more efficiently. Combined with expanded vector and floating-point execution capabilities, it becomes particularly powerful for the kind of dense mathematical operations that underpin modern AI. In practical terms, it makes AMD chips increasingly attractive for AI inference.

As Nvidia focuses heavily on large-scale AI training, AMD is positioning Zen 6 as the chip of choice for inference workloads. Given that inference represents the majority of real-world AI usage, this is a smart strategic bet.

Cracking the CUDA Wall: ROCm 7

Nvidia’s deepest competitive advantage has never really been its hardware. It’s been its software. CUDA, Nvidia’s programming platform, has been refined over nearly two decades. Millions of developers know it. Every major AI framework is optimised for it. Switching away from CUDA has historically meant rewriting enormous amounts of code, which is why so many organisations have stayed on Nvidia hardware even when alternatives existed.

ROCm 7, AMD’s answer to CUDA, is beginning to change that calculation. AMD’s Instinct MI300X running ROCm 7 delivers more than 3.5 times the inference performance of its predecessor. More importantly, ROCm 7 now supports the latest low-precision formats (FP4 and FP6) that are essential for efficient large-scale AI inference.

Two developments make ROCm 7 more than just a technical update. First, AMD has expanded the platform to support Windows and consumer Radeon GPUs, meaning developers can now build and test AMD-compatible AI software on their personal computers. This builds the kind of grassroots developer familiarity that has always been CUDA’s greatest strength.

Second, Microsoft is now offering toolkits that automatically convert CUDA code to ROCm-compatible code. This dramatically lowers the switching cost that has kept enterprises tethered to Nvidia. If you can migrate your existing software without a complete rewrite, the barrier to trying AMD hardware drops significantly.

AMD’s goal is to reach 15% market share in AI accelerators by the end of 2026. ROCm 7 is the software foundation that makes that target plausible.

Real Risks: What Could Go Wrong

AMD’s momentum is real, but so are the headwinds. Investors and observers should keep a close eye on several structural risks that could slow the company’s trajectory.

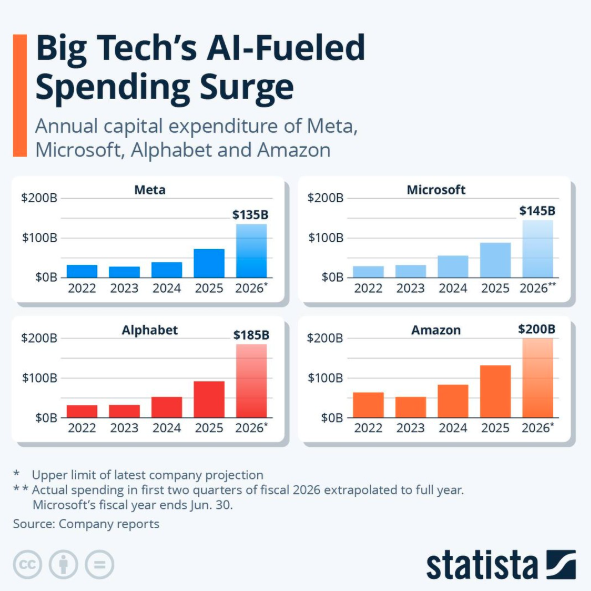

The most pressing is what might be called the capex cliff. The four largest hyperscalers Amazon, Google, Microsoft, and Meta have collectively planned around $700 billion in capital expenditure for 2026. That figure exceeds their combined operating cash flow, raising legitimate questions about how long such spending can be sustained. If the buildout slows, AMD’s order book could thin quickly.

Power is also a genuine bottleneck. Data centers require enormous amounts of electricity, and grid infrastructure in many regions isn’t keeping pace with demand. Projects are already being delayed due to power shortages, which could push back the timelines on AMD’s largest deployments.

Finally, there’s the custom chip threat. Meta is also exploring Google’s TPUs as an alternative, and both Meta and Microsoft are developing in-house AI chips. The more hyperscalers build their own silicon, the less room there is for both Nvidia and AMD.

The Bigger Picture

The AI hardware market is undergoing a genuine structural shift. For the past several years, Nvidia has operated something close to a monopoly on high-performance AI compute. That era isn’t over , Nvidia remains the gold standard for frontier model training, and its ecosystem advantages are still formidable. But the conditions that allowed that monopoly to persist are eroding.

Hyperscalers don’t want single points of failure in their infrastructure. AI labs don’t want to be entirely at the mercy of one supplier’s pricing and availability. And now, with AMD offering competitive hardware, a maturing software stack, and creative partnership structures, there’s a credible alternative for the first time.

The question isn’t whether Nvidia will survive.. it will. The question is whether the AI compute market can support two major players, or whether it will fragment further into a world of custom silicon and in-house chips. What seems clear is that the monopoly phase is ending, and AMD has done more than any other company to bring that moment about.