The transition from a high-growth startup to a profitable media titan is a rare feat. As of 2026, Spotify’s consistent profitability and fortress balance sheet provide the proof-of-concept necessary for investors to re-examine the business. The core question has shifted: it is no longer “Can they make money?” but “How efficiently will they deploy it?” Amidst the current AI surge, the ultimate test for the new leadership will be whether they fall prey to superficial marketing stunts or successfully integrate legitimate, value-driving AI applications into their existing ecosystem.

If you are considering adding Spotify (SPOT) to your portfolio, consider their expansion strategy, and the new leadership team tasked with navigating the “Year of Raising Ambition.”

1. Spotify Business Model

Spotify operates as a two-sided marketplace. Its core value proposition is balancing the needs of two massive stakeholders:

- The Supply: Music rights holders (major labels like Universal, Sony, and Warner, plus thousands of independents).

- The Demand: Listeners seeking a seamless, personalized audio experience.

The logic is straightforward: Spotify’s primary business is a “pass-through” engine. To grow, they must either increase the total pool of money coming in or increase the “efficiency” of the money they keep.

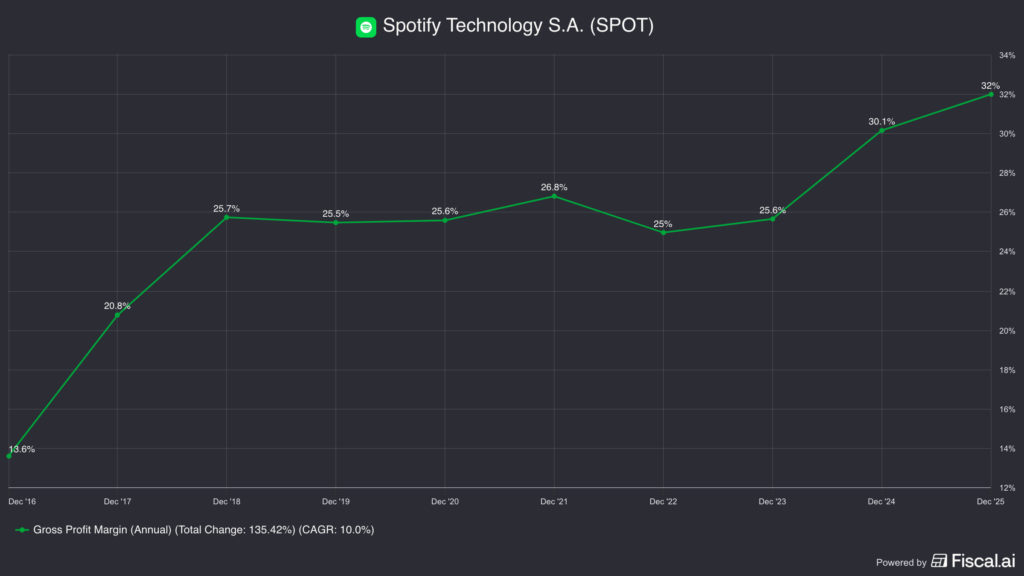

Gross Margin Expansion: Historically, Spotify kept about 25–30% of every dollar. In 2025, they pushed this toward 32%. This happens not by paying artists less, but through “Marketplace” tools where labels pay Spotify for better promotion, essentially giving Spotify a larger “cut” of the revenue.

The “Funnel” Efficiency: 60% of Premium subscribers start as free users. (Standard SaaS Free-to-Paid Conversion is 1-2% with Dropbox gold standard of 4%) Spotify’s ability to convert “ad-supported” listeners into “subscribers” is the single most important predictor of long-term revenue, as Premium users are significantly more profitable.

Understanding this “70/30” split is vital. If Spotify can move the needle to a 75/25 or 60/40 split through product innovation and negotiation, the impact on their bottom line is exponential.

Pricing Power and Stability

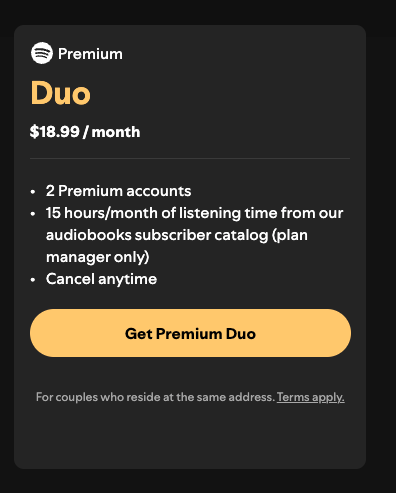

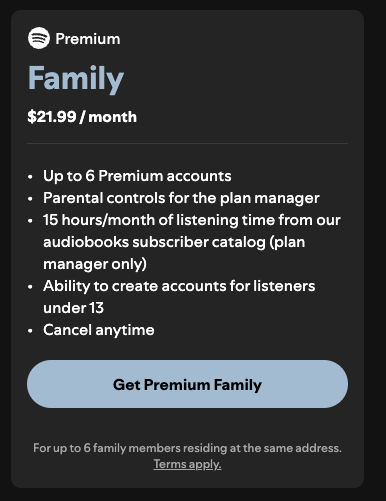

The “family plan” and “duo” tiers remain the company’s most effective retention tools. By bundling multiple users into one account, Spotify creates high switching costs; it is difficult for a family of six to migrate their individual tastes and playlists elsewhere. In early 2026, Spotify continued its trend of incremental price hikes in the U.S. and Europe. The fact that user churn remains near record lows despite these hikes proves Spotify’s immense pricing power.

2. The Financial Engine: 2025 Performance

2024 was Spotify’s “Year of Efficiency,” but 2025 was the year it proved that profitability is sustainable.

- User Scale: As of Q4 2025, Spotify reached 751 million Monthly Active Users (MAUs), an 11% increase year-over-year despite price hikes.

- Premium Growth: Subscriptions reached 290 million, providing a predictable, high-margin revenue stream.

- Profitability: With Q4 2025 revenue hitting €4.5 billion, Spotify has maintained its streak of positive operating income.

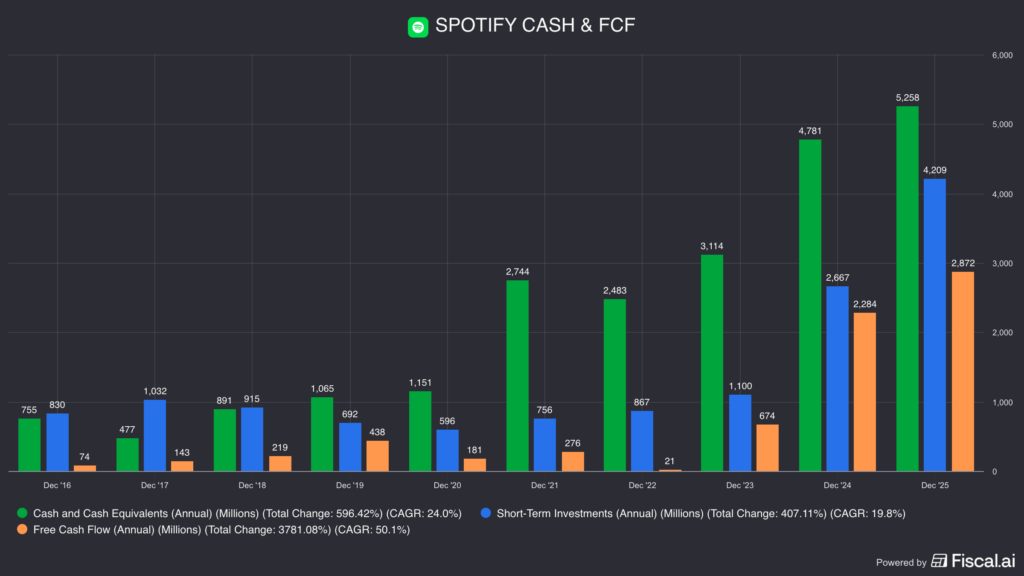

- The War Chest: The company generated €2.9 billion in free cash flow in 2025. With nearly €10 billion in cash on the balance sheet, the focus for 2026 has shifted from survival to capital allocation.

3. Expansion into New Formats

To justify its valuation, Spotify is moving beyond being just a “music app.” They are aiming to own the entire “earshare” of the consumer.

The Physical Book Market

In a surprising move, Spotify entered the physical book market in early 2026. Through a partnership with Bookshop.org, users can now discover an audiobook and purchase the physical print copy directly through the app.

The Strategy: This solves “consumer friction.” Instead of leaving the app to go to Amazon, Spotify acts as the discovery layer. This is a “capital-light” model—Spotify earns affiliate fees without the headache of managing warehouses or logistics. the effectiveness of the affiliate fees revenue is never to earn more free cash flow, but to create stickiness with subscribers.

Video Podcasts: The YouTube Challenger

Video podcast consumption increased by over 90% following the launch of the Spotify Partner Program.

There are now over 530,000 video shows on the platform. Unlike YouTube, Spotify offers a seamless “background play” experience. You can watch the video on the train, lock your phone, and continue listening via Bluetooth without the video stream cutting off—a feature that remains a friction point on other platforms.

4. Leadership Deep Dive: The Co-CEO Era

The most significant change for investors to track is the leadership transition effective January 1, 2026. Daniel Ek has moved to Executive Chairman, leaving the day-to-day operations to two long-time lieutenants.

Alex Norström (Co-CEO, Business)

Norström is a veteran of King.com (the makers of Candy Crush) and has been at Spotify since 2011. He is a master of the “Freemium” funnel. He oversaw the growth strategies that took Spotify from a niche European service to a global powerhouse.

Focus: Subscribers, advertising, and licensing. His background in gaming helps Spotify think about monetization loops and how to squeeze more value out of every minute a user spends in the app.

Gustav Söderström (Co-CEO, Product & Tech)

Söderström joined in 2009 and has been the architect of Spotify’s product DNA. A serial entrepreneur who sold companies to Yahoo and Facebook, Söderström is the reason Spotify’s recommendation algorithm is considered the gold standard.

Focus: Engineering, AI integration, and platform innovation. He is currently spearheading “Page Match,” a feature that allows users to scan a physical book page and jump to that exact spot in the audiobook.

5. Why This Structure Works

In this “mature” stage of Spotify, the company needs to execute on two fronts simultaneously:

- Technical Innovation: Maintaining an edge over Apple and Google.

- Business Optimization: Negotiating better margins with labels.

By splitting these duties, Daniel Ek can act as the “Coach” (Executive Chairman), focusing on long-term capital allocation—deciding whether to buy back stock, acquire new companies, or enter new markets—while the Co-CEOs run the weekly “eTEAM” to ensure the machine remains synchronized.

6. Investor Verdict: Should You Buy?

Spotify is no longer a “speculative” tech stock; it is a utility for culture. Its massive data advantage and solid balance sheet make it a formidable player. The bull case rests on their ability to turn “video” and “books” into high-margin segments that rival their music business.

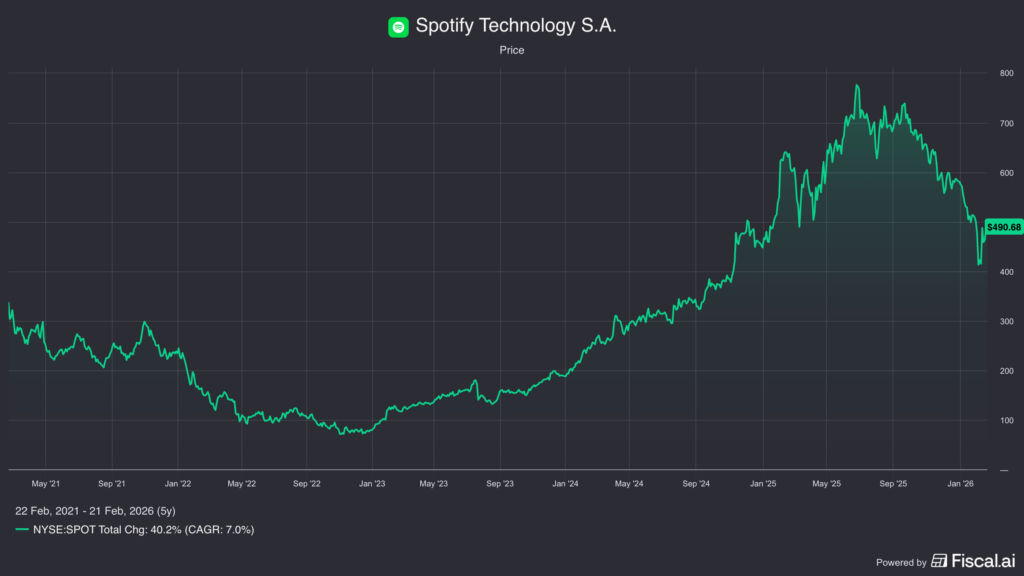

Spotify has pulled back significantly from its all-time highs, caught in a broader sell-off alongside legacy media giants like Netflix and Disney. These companies are currently being sidelined as “non-AI plays” by investors chasing the latest “shiny objects” in the tech sector.

However, for those seeking to diversify away from pure-play AI volatility, Spotify warrants a second look. Supported by a strong balance sheet and a competitive moat that remains incredibly difficult to breach, the company offers a rare combination of stability and untapped scale. While the market is distracted by infrastructure hype, Spotify is quietly leveraging its dominant market share to become the undisputed utility of the “audio economy.”